2025 will be remembered as the year data centre grid independent microgrid power came of age and how GWs of provision of renewable energy for data centres at scale changed for good.

Hyperscalers such as Amazon, Google and Microsoft and major colocation operators have made huge data centre sustainability strides in terms of behind the meter efficiency, utilisation and performance, while working hard to be good grid citizens through investments in PPAs and renewable energy guarantees of origin certificates (REGOs). They have also made significant direct investment into solar, wind, hydrogen and other sustainable energy technologies.

And it is not just the hyperscale and commercial operators who are seeking power for data.

Every government is at pains to promote its AI and digital economy strategy built around sovereign and sustainable data centre capacity. But each knows that it cannot risk adding additional strain to national grids that are in transition and, already experiencing surging demand. The development of microgrid energy solutions for data centres is recognised as key to AI success.

Such is the unprecedented appetite for data centre infrastructure that a seismic shift in how power is accessed is underway. There is a supply side scramble for suitable locations in or close to the traditional tier 1 European markets (Frankfurt, London, Amsterdam, Paris and Dublin), in rapidly evolving tier 2 cities (Milan, Madrid, Berlin, Warsaw, Zurich, Athens et al) and further afield. Every investor, developer, real estate expert, site acquisition professional, and M+E design engineer is faced with the same set of power questions.

“Where is the power?” “How much can I get?” “What are my grid connection options?” “What is the connection timeframe?” “Where is the closest renewable generation?” “What are my net zero energy solutions options?” “How can I measure and prove my green power and sustainability credentials for zoning, development planning, construction and decades of operation?” “Can I develop and operate digital infrastructure that is green and economically viable?”

Increasingly the answers to these questions are not to be found in securing connections to already constrained grids. Faced with lengthening connection queues, developers are pivoting to viable off-grid solutions and embarking on detailed evaluation of private wire power generation and microgrid options to meet AI energy demands.

The context is global data centre capacity demand curve estimated to be around 50 GW as of 2023 and is predicted to rise to 200 GW by 2030, with AI accounting for 15% of this demand in 2023 and predicted to account for 40% by 2030

This is sparking a change in how future data centre developments are being planned across Europe.

The power of data

A new technical whitepaper from the UK’s Loughborough University, Centre for Renewable Energy Systems Technology (CREST) is helping operators evaluate the true economic and carbon cost of grid independent microgrid development and operation.

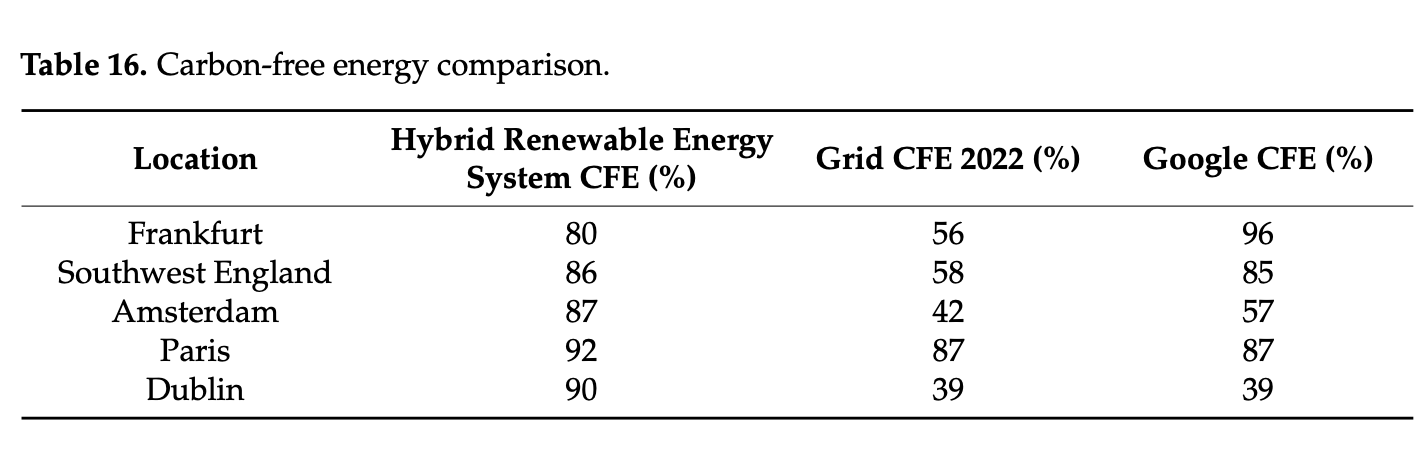

Called Technoeconomic Feasibility of Wind and Solar Generation for Off-Grid Hyperscale Data Centres it is aiding data centre operators by providing a true carbon and economic cost picture of grid independent operation over a 35-year operation for data centres across the FLAP+D (Frankfurt, London, Amsterdam, Paris, Dublin) tier 1 markets.

The paper provides developers looking at their grid independent, renewable hybrid microgrid options with actionable comparison data and insight on ‘the costs and carbon emissions associated with stand-alone hybrid renewable and gas generation microgrids that could be deployed either before a grid connection is available, or to allow the data centre to operate entirely off-grid.’

It shows that off-grid generation could provide both lower cost and carbon emissions for each of Europe’s major data centre hotspots.

It says: ‘This paper presents a solution..[to power access] challenges by deploying hybrid renewable energy systems for providing off-grid energy to data centres…This approach uses wind, solar, gas and batteries to provide reliable and sustainable energy to data centres that cannot obtain a connection to local grids…It compares each generation configuration to grid equivalent systems and an onsite gas-only generation solution. The results showed that each hybrid renewable generation configuration had a reduced levelised cost of energy (LCOE) and reduced CO2eq emissions compared to that of its grid and gas-only equivalent.”

Demand curve forecasts show the energy consumption associated with global data centre capacity demand (as estimated by the International Energy Agency (IEA)) as set to rise to 1000 TWh by 2026 from 460 TWh estimated in 2022 and is expected to rise from 1% to 6% of the UK energy demand by 2030.

Alongside such huge demand additional impetus for the consideration of independent data centre power is the fact that Europe has some of the oldest power grid systems in the world. The average age of Europe’s grid transmission systems is almost 50 years.

Add to this that amid a race to build sufficient renewables at scale, each country is faced with retiring fossil fuel power stations, the forementioned creaking grid systems, a decade long wait for connections in some locations, and an equally long wait for new technologies such as Small Modular Reactors and green hydrogen.

The data centre industry is not alone in feeling the impact of long-term insufficient investment in grid infrastructure that is leading to increasingly constrained systems.

The paper says the impact is twofold. “It is starting to slow the progress of the deployment of renewable energy, (over 3000 GW of renewable generation projects awaiting grid connections as of 2023). And constraints are also inhibiting the construction and operation of new data centres.”

As they seek to attract investment in and development of data centres, governments know they must be seen to stick to their green energy transition and net zero commitments within stated timeframes even as the competition for power from mass electrification of industry and transport surges.

Renewable Off Grid Metrics for Success

The challenge faced by the data centre sector is how to sustainably deliver energy to a new industry that is growing at such a rapid pace.

The whitepaper proposes that short, medium and long term operation of data centres at scale will require off grid, private wire, on-site generation capabilities at an economic and carbon cost that is provably lower than traditional grid power.

The paper considers a solution to this challenge as the deployment of hybrid renewable energy systems providing off-grid energy to data centres using wind, solar, gas and batteries to provide reliable and sustainable energy to sites that cannot obtain a connection to local grids. (The waiting time for a grid connection in the UK is 8-10 years, while countries such as Ireland and the Netherlands have effectively banned new data centres that need grid connections.)

Until now there has been little solid information on the cost, carbon emissions and measurable impact of a data centre that uses renewables, gas turbines generators and batteries in a stand-alone hybrid renewable and/or gas generation microgrid to allow the data centre to operate entirely off-grid.

The paper addresses the optimal configurations with wind and solar generation, backed up by battery storage and onsite gas generation for data centres in Frankfurt, London, Amsterdam, Paris, and Dublin.

The results of the optimum hybrid renewable energy system at each proposed location are for a 50 MW constant load hyperscale data centre with an expected operational life of 35 years.

In the case studies the paper compared combined renewable and gas generation microgrid configuration to grid equivalent systems and onsite gas-only generation solutions.

Using LCOE the results show that “off-grid generation could provide lower cost and carbon emissions”

It provides strong evidence that data centres using renewable microgrids produce less carbon than those relying solely on grid connections. It assesses real world scenarios, taking into account the longer development cycles for renewable power sources, and the need for natural gas generation as a bridging and back up energy source.

With labels such as ‘medium’ and ‘hyperscale’ data centre currently considered in the range of 30MW to 300MW the study focuses a flat load profile of a 50MW facility – while acknowledging that data centres reach full load over time. Unlike previous studies the results address the economic mismatch between generation and consumption.

To this end the paper also introduces ‘a new metric to evaluate and compare the economic performance of each microgrid. Called the levelised cost of energy utilised (LCOEu) it gives the levelised cost of energy for a given microgrid considering only the energy which is consumed by the data centre. The LCOEu across all sites was found to be between 70 and 102 GBP/MWh with emissions between 0.021 and 0.074 tCO2eq/MWh.’

For comparison purposes, the results showed that each hybrid renewable generation configuration had a reduced LCOE and reduced CO2eq emissions compared to that of its grid and gas-only equivalent. The LCOE is the average cost (MWh) taking the total lifetime costs and dividing by the amount of energy produced over that lifetime.

To provide a fair comparison including utilization the LCOEu metric provides a definition of the energy utilization of the data centre over a lifetime of operation (which is a higher value than LCOE alone.)

By providing deep technical evaluation of hybrid schemes of solar and wind farm configurations (because such renewables are readily available onshore in Europe), battery energy storage systems (also available and scalable (unlike green hydrogen), alongside natural gas power generation and locations (land prices) the paper provides actionable data on power costs, carbon footprint of standalone hybrid renewable microgrids.